'Tis Only My Opinion!™December 2015 - Volume 35, Number 12"Outlook 2016""Peering into a Crystal Ball"On December 16th, at the Federal Open Market Committee (FOMC) meeting the Federal Reserve (FED) raised the Federal Funds Rate by whopping 0.25%, or 25 basis points. The equity markets responded initially with an exuberant reaction for the balance of the trading day. During Janet Yellen's press conference following the FOMC's rate hike decision, a picture of an improving economy with an unemployment rate of 5% was painted along with hope for improvement in other areas of the economy as the primary reasons for the December 16th rate hike. However, I believe there might have been another reason. If the Federal Funds Rate was left unchanged, the FED would lose credibility with bond market investors and other sovereign central banks. As we peer into the crystal ball, we will try to ascertain whether the FED's Outlook is correct. However, the reaction of the markets during the two days following the FOMC decision was less than exuberant as traders and investors sold stocks heavily. The implications of further interest rate hikes during 2016 must be considered in any analysis of the conditions facing the economy going forward. We believe that to make any forecast about the future will require an understanding about not only the current world economic conditions but also about the "Four D's" and how they will impact various interacting forces.

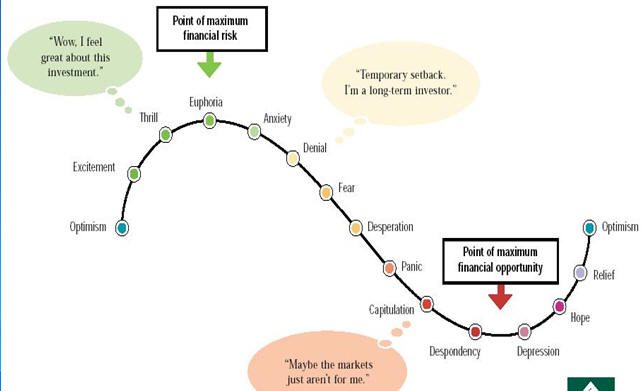

Where are We?In attempting to make a realistic forecast, it is helpful knowing where the economy is in the investment and economic cycle. Ms. Yellen along with the FED's economists probably believe the U.S. is at the point labeled "Hope" on the following graph. However, "Denial" seems more likely to me.

The Four "D's"Also, in making a realistic forecast, the current status and possible change in the "Four D's" must be considered. The four D's are:

Peering into the Crystal BallAs we look into the crystal ball, we will try to show how statistics revisions can change, or manipulate, the public's perception of the real world. We will also point out those demographics which may be important in the short and long run for the nation. Finally, we will briefly discuss the impact of the International Monetary Fund's (IMF) recent decision to include China and India in their basket of currencies and how this might impact the dollars' run as the world's reserve currency.

Demographics

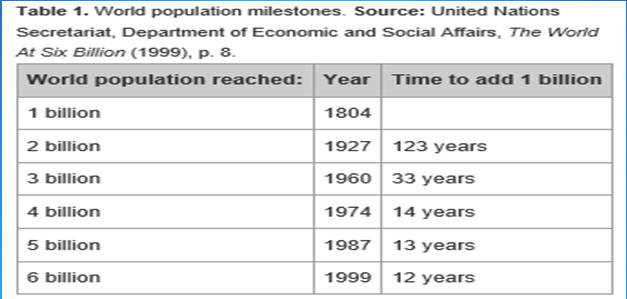

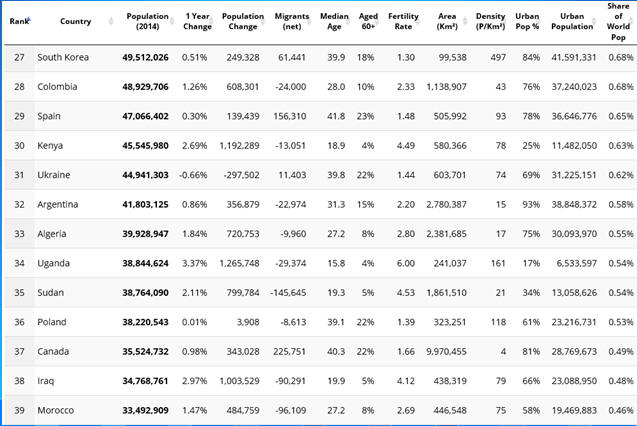

Demographics is simply the study of various factors in a data set to ascertain how changing conditions can impact the future. Table 1 points out the growth of world population and the significantly shortening of the time to add another billion people.

Important demographic considerations are:

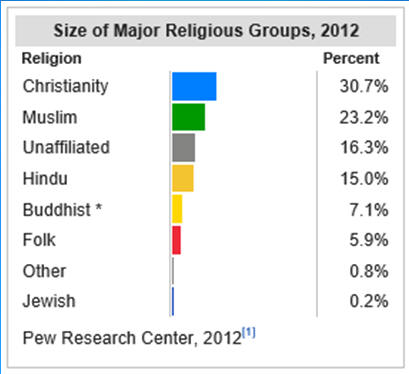

The Pew Research Center in 2012 did a study of the World Population by Religion, the results of which are shown in the following graph.

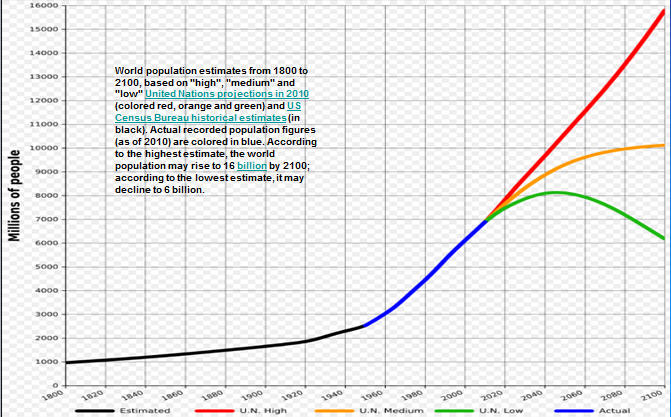

The following graph from the United Nations "World Population Estimates, The 2015 Revision" illustrates not only past and current growth of world population but future growth through the year 2100 using various estimates. The highest estimate is that the world population will continue to increase to about 16 billion people while the lowest estimate suggests that various factors will contribute to an actual reduction in the current level of world population.

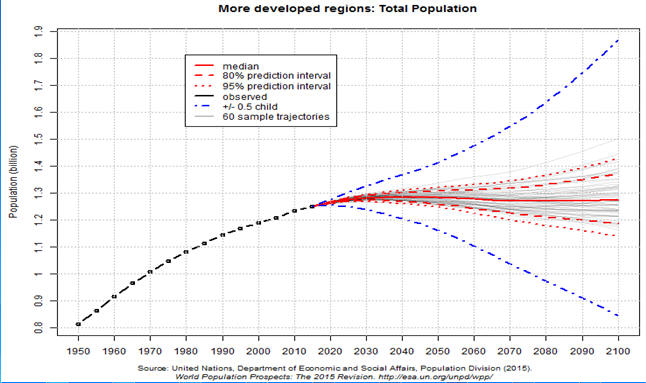

The United Nations also projects population growth among the more developed regions as shown in the following graph. What is striking is that the fertility rate will probably cause those regions to stagnate or actually decline.

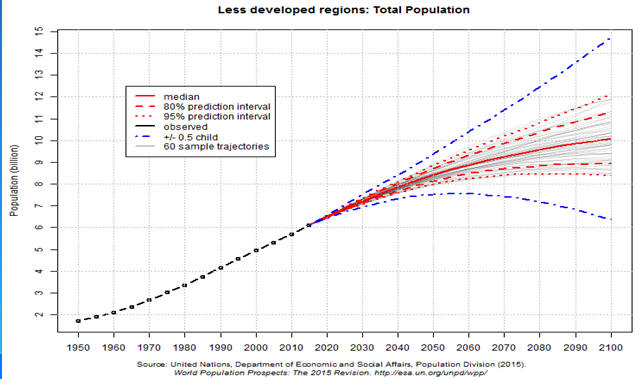

Because of a higher fertility rate in the less developed nations, the UN projections suggest that much of the population growth through 2100 will occur in those regions.

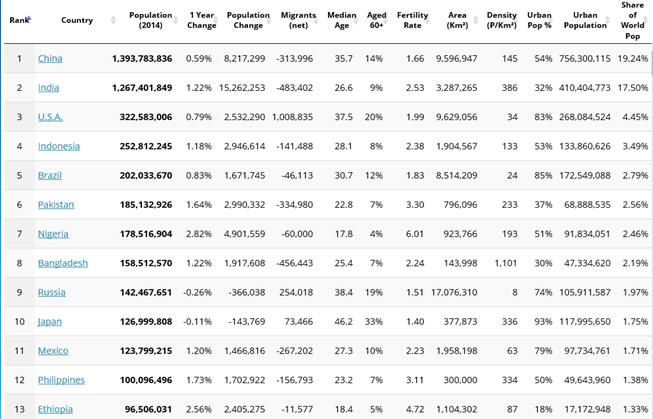

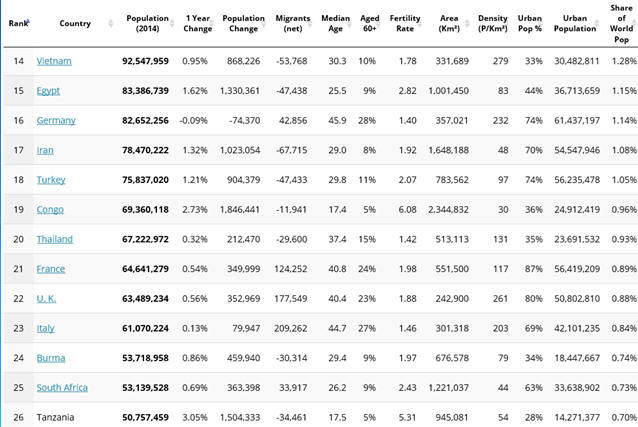

Various country statistics from the United Nations regarding demographics are shown below. By comparing the population density, fertility rates, number of migrants and the percentage of the population over 60, the reader will understand the problems facing many of the countries in the global economy.

In the long run, demographics will determine the economic, political and strategic changes in the local, national and world economies.

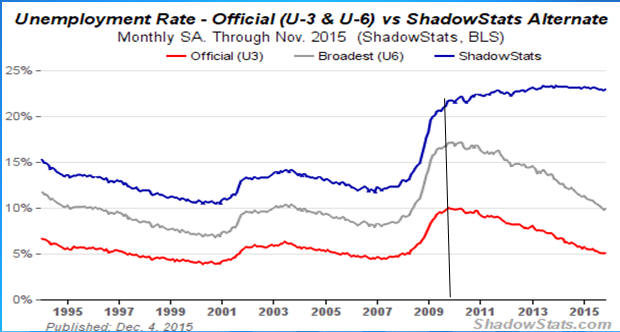

Debt & the Federal Reserve SystemThe Federal Reserve System according to its enabling legislation has three mandates: 1. Maintain maximum employment 2. Provide stable prices (defined currently as a 2% inflation target.) 3. Provide for moderate long-term interest rates. Certainly, the FED cannot claim to have maintained maximum employment when Shadow Government Statistics (SGS) suggests that unemployment is currently running at 22.9%, nor did the FED provide "moderate long-term interest rates" which rose to over 15% in 1979 as seen in the following chart of the 10-year U.S. Treasury note.

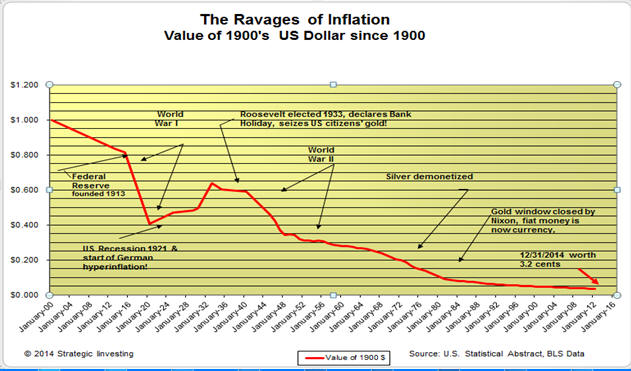

The FED's belief that stable prices means a 2% inflation target is simply another way of inflating the debt away by stealing from the citizens of the U.S. A 2% inflation rate implies that the FED wants to confiscate about 18% of each person's net worth during the coming decade. The track record of the FED is less than stellar. Why Congress failed to terminate its charter in 2013 is beyond my understanding. The FED has presided over a monetary system which began to change to a fiat system beginning in the 1930's under President Roosevelt. The value of each dollar which was worth about 80 cents when the FED came into existence has been inflated away to become worth only about 3 cents in the 80 years of its existence.

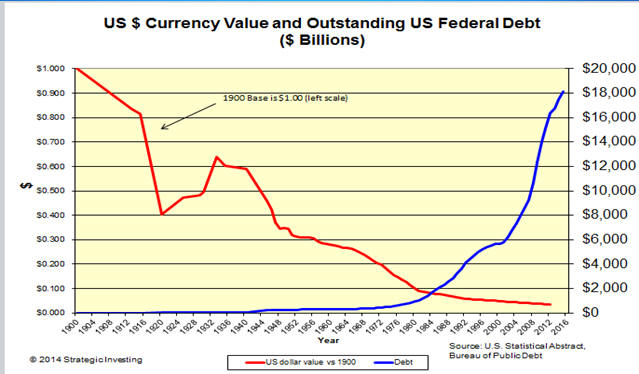

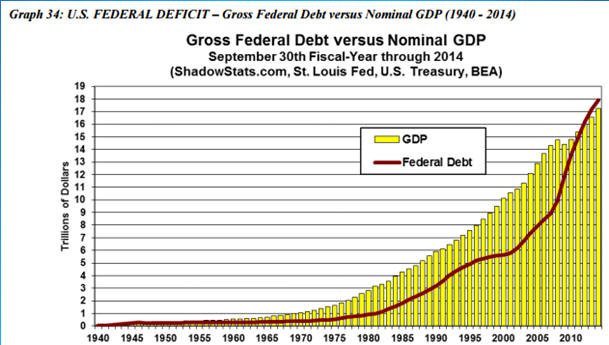

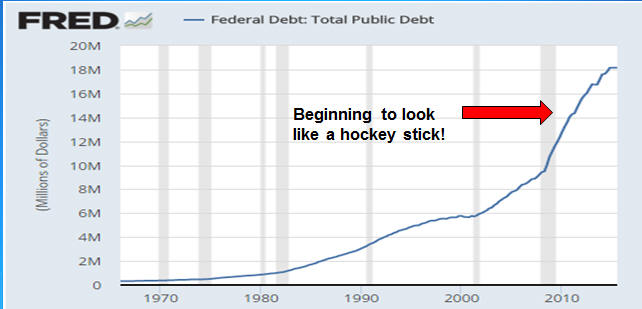

As the value of the dollar declined, the Outstanding U.S. Total Federal Debt rose as seen in the following chart.

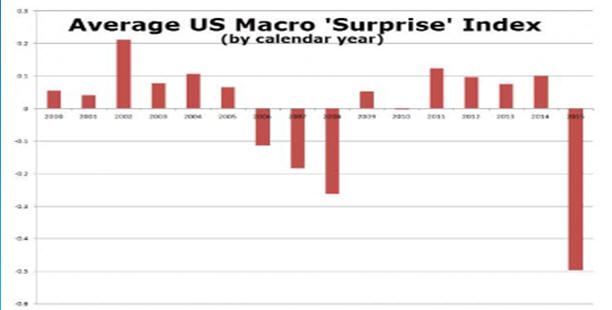

The policies of the FED will increase both inflation and deflation dramatically in the short run. This is largely because the FED's policies were based upon expectations which have been significantly in error. The following graph shows the record of their yearly forecasts for the economy since the year 2000.

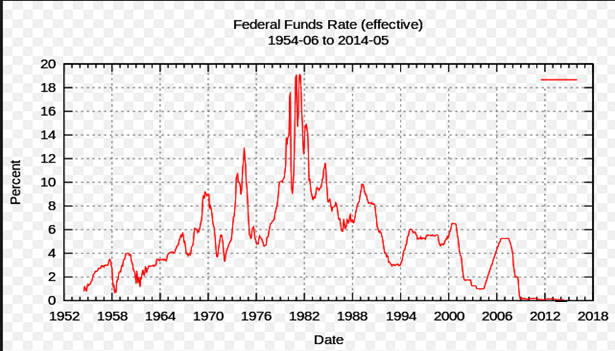

The Federal Funds Rate has fluctuated since 1954 as shown in the following graph. It reached a high of 19.5% in 1981 under Chairman Volker when he was attempting to break the inflation cycle. For the seven years prior to Wednesday's increase, the Federal Funds Rate was at historic lows.

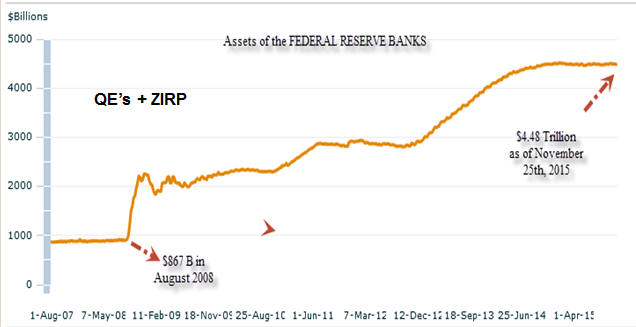

Following the closure of the two Bear Stearns funds in June 2008 and the collapse of Lehman Brothers on September 14. 2008, the FED in conjunction with the U.S. Treasury started a rescue program of the U.S. financial system which AIG was about to blow up. The FED acquired assets of questionable quality as well as acquiring a substantial portion of the outstanding long-term U.S. Treasuries. Policies were initiated including Quantitative Easing (QE) and Zero-Interest-Rate Programs (ZIRP) programs which have ballooned its assets from $867 billion to $4.487 trillion as of November 27, 2015 as seen in the following graph.

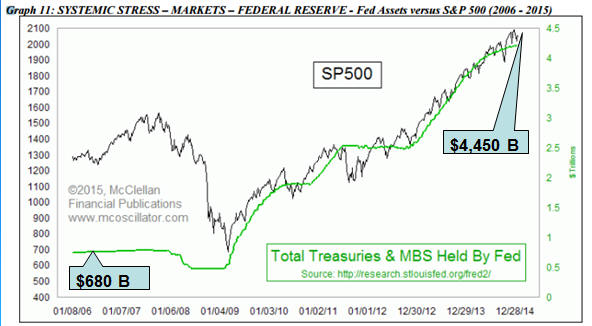

The high correlation between the growth of the FED's assets and the increase in the S&P 500 index is shown in the following graph.

The stock market has enjoyed a seven-year bull market thanks to the FED's QE and ZIRP programs as seen in the next two graphs of the NASDAQ and the S&P 500. However, the bull market is showing signs of trending down.

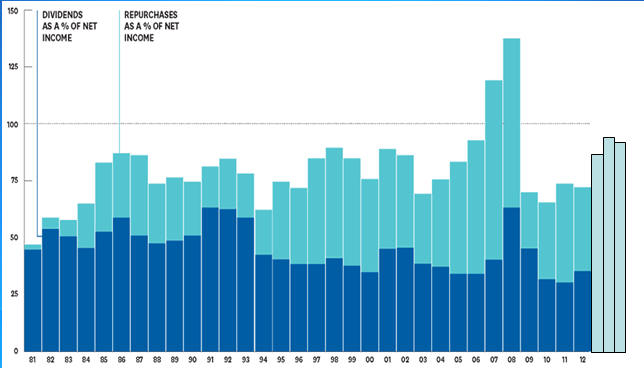

Dividends & Buybacks reduce U.S. Competitiveness & Research and DevelopmentDuring the past seven years, a significant portion of corporate profits have been used to pay dividends and more importantly, to fund stock buybacks as seen in the following chart. The amount of corporate funds available for infrastructure upgrading and research and development expenditures has hence shrunk which in the long-run has reduced the nation's ability to compete globally. Dividends and Stock BuyBacks as a % of Corporate Profits

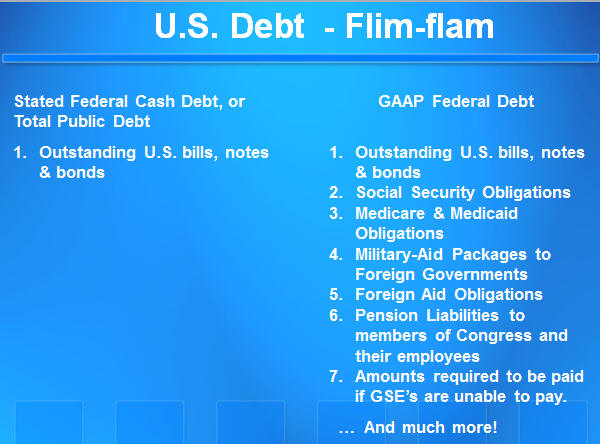

The U.S. Dollar is under AssaultIn Janet Yellen's press conference following the rate increase, many pundits concluded that the FED may raise interest rates twice during 2016 and each time by 0.25%, or 25 basis points. However, if the rationale for raising interest rates is to reload the FED's ability to assist the economy, it might raise the Federal Funds Rate by 0.50%, or 50 basis points, each time in my opinion. It is highly likely that the FED will come under increased review by Congress in 2016 or 2017. Many bankers and politicians throughout the world are simply tired of the U.S. using the dollar's reserve status to enable it to be the only world's superpower. In fact, China has developed trade pacts with most of its major trading partners. China has at least 26 swap agreements including Brazil, Canada, Russia, the ECB, United Kingdom, Malaysia, Qatar, Iran and Pakistan. Swap agreements reduce the reliance of the U.S. dollar as a medium of exchange. The World Bank is an international financial institution that provides loans to developing countries for capital programs. It comprises two institutions: the International Bank for Reconstruction and Development (IBRD), and the International Development Association (IDA). The World Bank is a component of the World Bank Group, which is part of the United Nations system. To compete with the World Bank which the BRICS believe is dominated by the U.S., they are in the process of funding a development bank initially with a $50 billion capitalization to compete with the World Bank. The BRICS bank would use $50 billion of seed capital shared equally between Brazil, Russia, India, China and South Africa but would undoubtedly be dominated by China. It would be the first institution of the informal forum which began in 2009 amid the economic meltdown to chart a new and more equitable world economic order. The clock is ticking on the dollar's role as the world's reserve currency and its demise will mean significant hardships for the American economy and its people. Moreover, don't be surprised, if the FED actually goes bankrupt by 2018. U.S. Debt - a Flim-Flam gameDuring the last century, the public's knowledge about what is really the amount of outstanding US government debt has been obfuscated by the politicians and a media that refuses to educate the public. Since 1990, the rate of growth in the Gross Federal Debt (Total Federal Debt) and Gross Domestic Product (GDP) has been changing. During this recent period, the growth rate of Total Public Debt has been increasing faster than GDP.

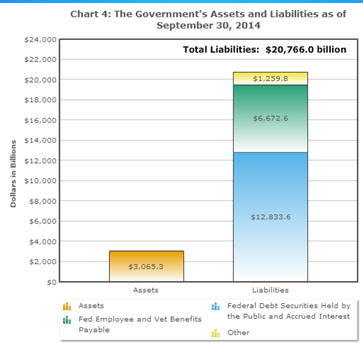

As of FY 2014, the U.S. Treasury pointed out that its Assets were only $3.065 trillion while is Total Liabilities stood at $20.7 trillion. Of course, that is "hogwash" as the amount of unfunded liabilities was not included.

In most discussions of the US government debt, what is portrayed as Total Public Debt is really simply the Stated Federal Cash Debt. The growth of Total Public Debt since 1960 has been remarkable and is beginning to take on characteristics of a hockey stick.

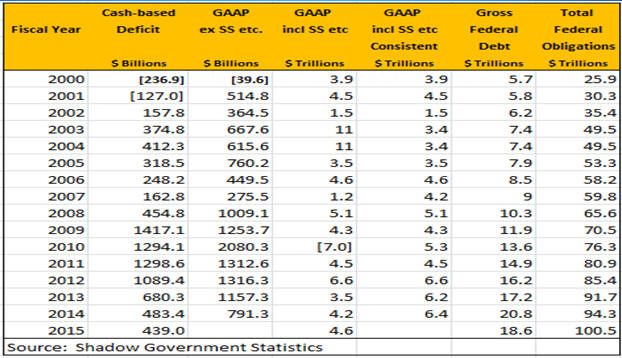

At the end of FY 2015, the Total Public Debt was estimated to be $18.7 trillion according to the U.S. Department of the Treasury. The following table shows some of the differences between the $18.7 trillion defined as Total Public Debt or Stated Federal Cash Debt and the actual GAAP debt of $105 trillion, or a 5X difference.

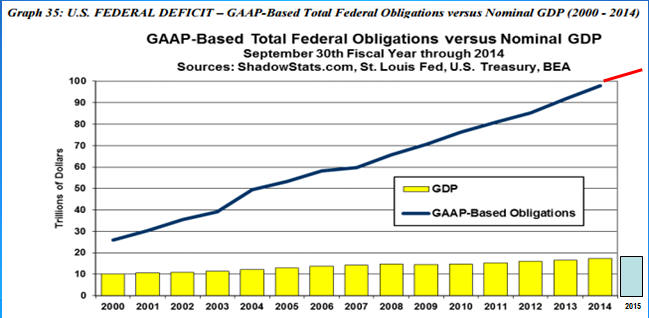

When you look at the real world, a totally different picture emerges as seen in the following graphs. The growth in U.S. Government Debt Obligations using Generally-Accepted Accounting Procedures (GAAP) versus the Cash-based Deficit reported by the U.S. Treasury and the complicit media is shown in the following table and graphs since 2000 courtesy of SGS.

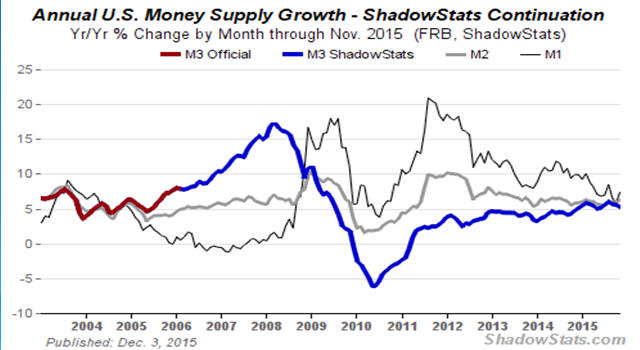

Just when the day of judgment will arrive is unknown, but many investors will be facing a lot of sleepless nights going forward. What is the definition of inflation?Inflation is simply an increase in the money supply without a similar increase in productive wealth, and not about a general increase in prices; it is about increases in the Money Supply. The following graph of M1, M2 and M3 illustrates the significant changes in each during the efforts of the FED to recapitalize the major money-center banks following Lehman's debacle.

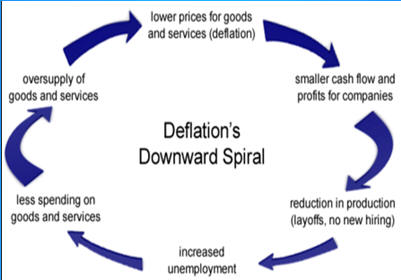

DeflationDeflation is a politician's worst nightmare. It can generate a downward spiral that leads to increased employment, less spending, lower tax revenues, and eventual bankruptcy for individuals, business, and governments.

The CRB Index which measuring a basket of commodities peaked in 2009 and is now at its lowest level since 1980 as seen in the following graph.

Corporate Profits since 2008 have benefited from financial engineering accounting. It is now showing the effects of a lack of top-line revenue growth and increased costs due to Obamacare and increased regulatory expenses. After-Tax Corporate Profits as seen in the Q3 report released in late November 2015 are beginning to roll-over.

Default?What are the options regarding the U.S. Debt going forward?The number of options are rather limited and most of them are not politically acceptable. Of course, the simple answer is to reduce spending and increase taxes. Politicians are wont to reduce spending by cutting social services including social security and public welfare programs. There is a substantial military/industrial complex that makes reducing military and/or defense spending difficult even when programs are no longer viable. Any attempt to reduce the number of government employees, their pay and benefits will be difficult thanks to civil service regulations and public-employee unions. Many federal programs have been started which are specifically not authorized by a strict reading of the Constitution of the U.S. But trying to get rid of the Education Department, for example, would be a monumental task. Politicians using the FED are attempting to inflate away the debt burden but a 2% inflation rate is simply not going to do the job. Whether the FED will be successful is doubtful. There are many things to ponder going forward which could create danger for not only the U.S. economy but the world economy as shown in the table. Things to Ponder

The Bank for International SettlementsMost investors have only a rudimentary knowledge of the existence of the Bank for International Settlements (BIS) in Basel, Switzerland. It is an immensely powerful international organization that most people have never even hear of which secretly controls the money supply of the entire globe. It is, in effect, the central bank to all the sovereign central banks like the FED in the U.S. BIS is expected to shortly authorize negative interest rates and account haircuts to depositors to attempt to prevent the financial collapse of sovereign central banks. In 2014, bank accounts in Cyprus were raided bankrupting many businesses and investors. Politicians, both here and abroad, have their eyes on the billions, if not trillions, of currency and monetary values residing in retirement accounts. Do not be surprised if portions, or all, of these accounts are confiscated to help offset a nation's debt obligations in a financial meltdown.

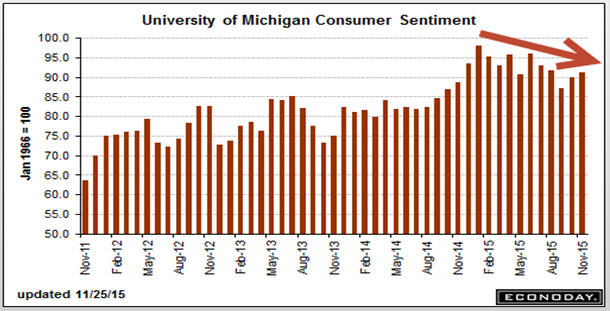

Economic IndicatorsThe U.S. EconomyAccording to many economists, Consumer Spending accounts for about 70% of the U.S. GDP. Hence, how the consumer feels about his/her prospects is very important and a gauge used to measure the health of the economy. Unfortunately, recent readings of Consumer Sentiment according to the University of Michigan are trending downwards as seen in the following chart.

Retail Sales are likewise in a downward trajectory as shown in the following chart. Hopes that the Santa Claus rally would rescue the economy appear to have been lost.

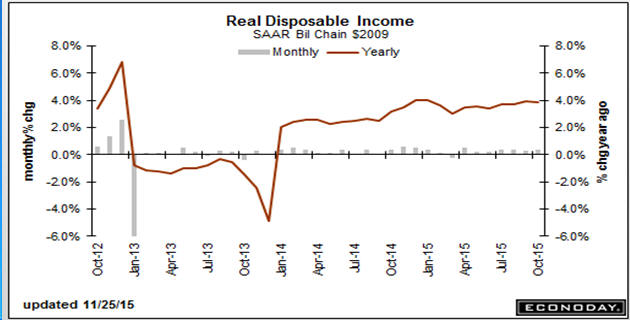

Of course, if Real Disposable Income does not show much improvement and is relatively flat when confronting increasing costs for insurance and taxes, it should not be a surprise if retail sales are not rising.

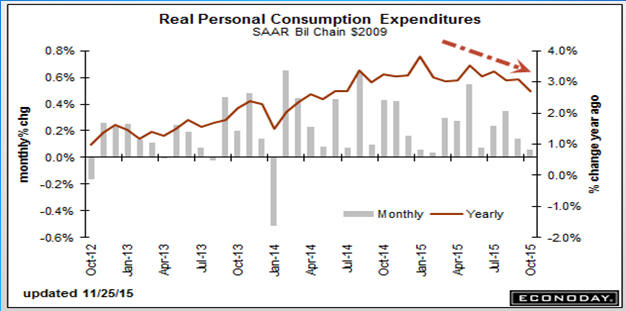

The consumer appears to be tightening their belts as shown in the following chart of Real Personal Consumption Expenditures.

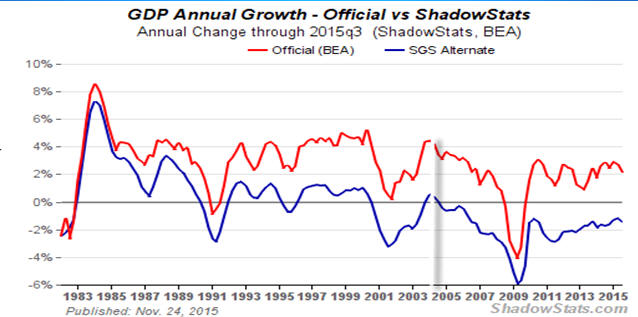

According to the Ministry of Truth (MOT), GDP is bumping along at about 2% growth. SGS points out that only by changing the methodology of computing GDP through the use of hedonic and substitution/addition elements does MOT show an economy growing at all. The following graph shows that the U.S. economy according to SGS actually entered recession in the 3rd quarter of 2004 and remains in recession.

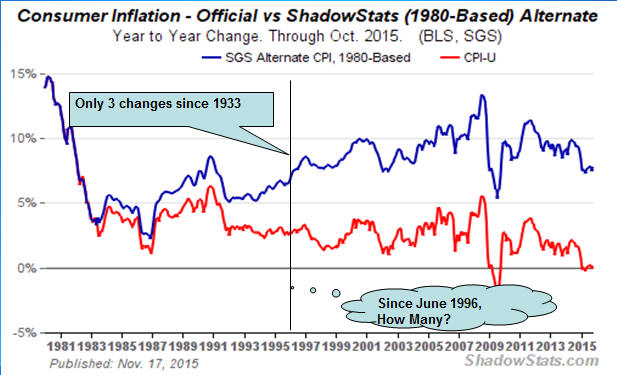

MOT's Consumer Price Index (CPI) is a can of worms which measures apples and pineapples and says that nothing has changed. MOT's CPI is almost zero. But. as the following graph shows, the CPI methodology was changed three times from its inception to June 1996. Do you know how many times it has been changed since June 1996?

The answer is 22 and in every instance, the reported CPI for the month in which the change was made was reduced. So much for honesty in government! Besides SGS, The Chapwood Index uses a slightly different approach to the calculation of GDP and CPI and the results since 2011 shown in the table below corroborate significantly the SGS data.

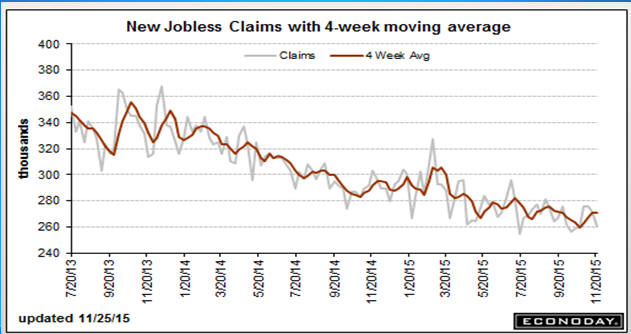

Unemployment & JobsAccording to MOT, New Jobless Claims appear to be stabilizing around the 260-280,000 level on a seasonally-adjusted basis.

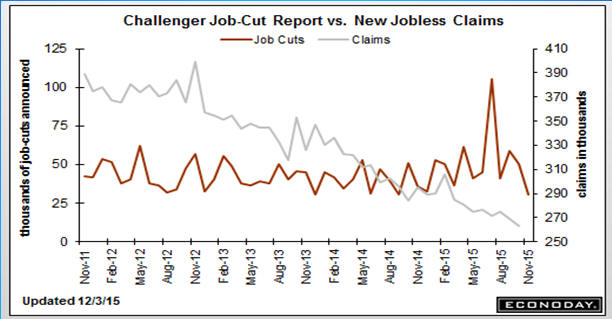

Corporate Layoffs appear to be declining as seen in the Challenger Job-Cut Report.

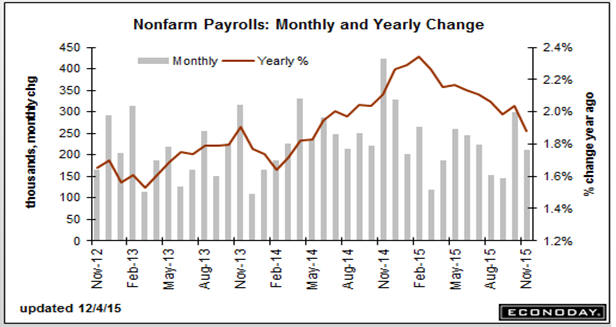

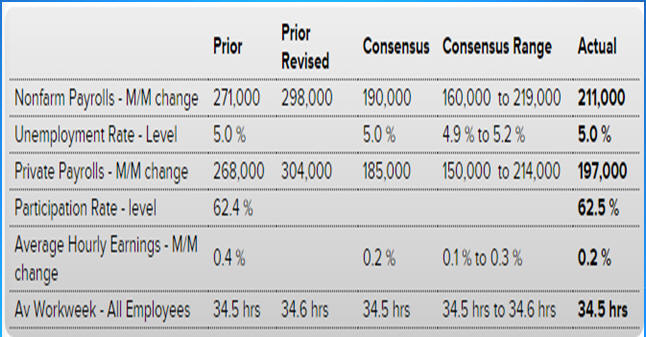

Monthly growth in Non-farm Payrolls is choppy with the recent trend being downwards. The November 2015 Jobs report showed a significant decrease.

While the October 2015 Non-farm Payroll was revised upwards by 27,000 to 298,000 jobs on a seasonally-adjusted basis, the November 2015 number was only 211,000. According to most economists, the economy requires the addition of 225,000 to 240,000 new jobs each month just to account for the increase in the population. November 15 Jobs Report

Obamacare was responsible for the increase in part-time workers rather than full-time workers with full benefits. As a result, if you dig into the November 2015 jobs report, the ugly and hidden truth behind the headline number is that full-time jobs are disappearing and part-time jobs are increasing. The real problem is that overall compensation of part-time jobs is less than the full-time job in most cases ... the result is a decrease in the amount of consumer income.

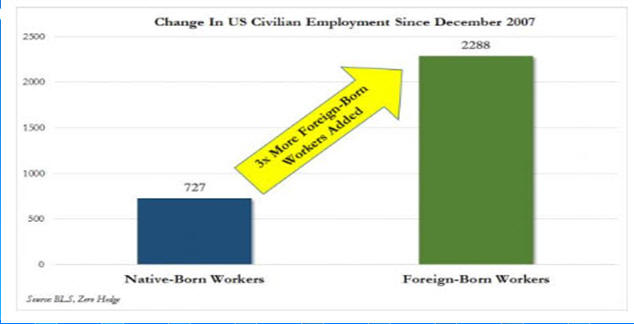

Analysis of the employment data also shows that since December 2007 Foreign-Born Workers have obtained almost 3 times the number of American jobs than Native-Born Workers as shown in the following chart.

Over the years, the MOT's Bureau of Labor Statistics has changed for political purposes, the methodology for calculating the Unemployment Rate. The widely-reported U-3 Unemployment Rate consists only of those people unemployed who have been looking for work during the past four weeks. For November 2015, the U-3 rate was 5.05%. The U-6 Unemployment Rate counts not only people without work seeking full-time employment (the more familiar U-3 rate), but also counts "marginally attached workers and those working part-time for economic reasons." Note that some of these part-time workers counted as employed by U-3 could be working as little as an hour a week. And the "marginally attached workers" include those who have gotten discouraged and stopped looking, but still want to work. The age considered for this calculation is 16 years and over. However, if a worker has been unemployed for more than a year, the worker is not counted in either the U-3 or the U-6 calculations. For November 2015, the U-6 rate was 9.90%. The SGS analysis of unemployment counts all people who have been unemployed and is the definition used prior to 1940. In November 2015, the real unemployment rate stood at 22.9%. Note that beginning in the last quarter of 2009, the relationship of the three unemployment series began to diverge.

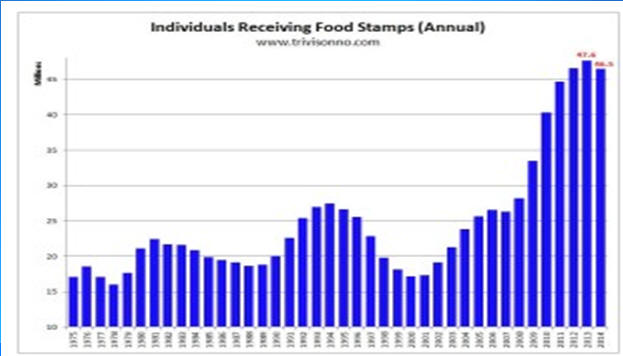

Welfare BenefitsIf the economy is healthy, why are so many individuals receiving Food Stamps as shown in the following chart.

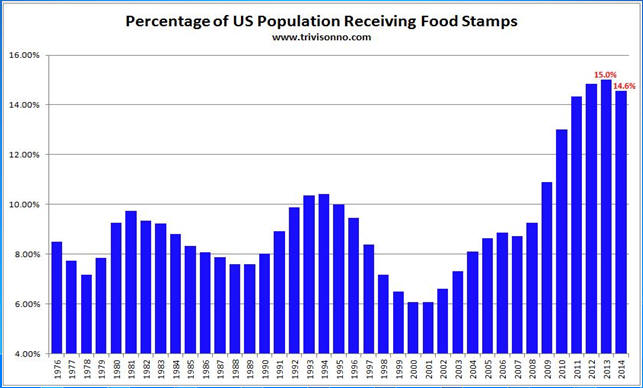

When almost 15% of the U.S. population is receiving Food Stamps, there is simply something wrong with our wage system.

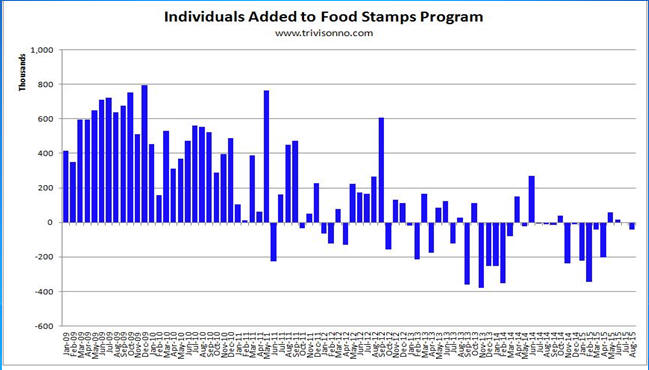

During the first years of the Obama Administration, there was a substantial increase in the number of individuals added to the Food Stamp Program.

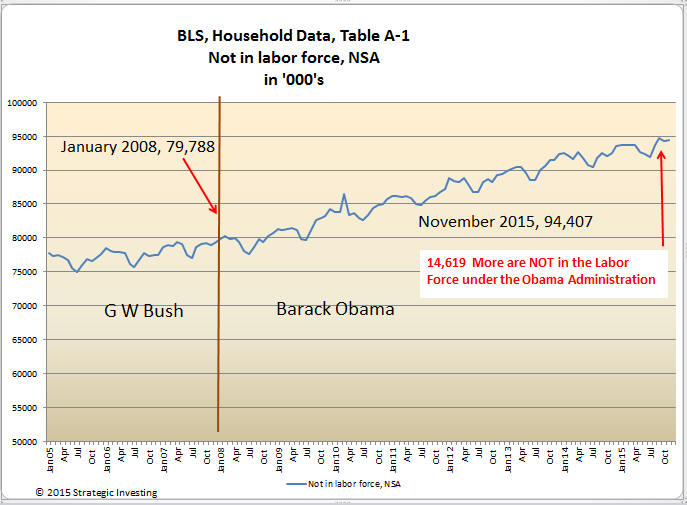

Coinciding with the increase in the Food Stamp Program was an increase in the Number of Individuals who were No Longer considered to be in the Labor Force. While some of this increase can be attributed to "Baby-Boomers" taking early retirement, the primary driver was the increased level of benefits available to those unable, or unwilling, to seek employment.

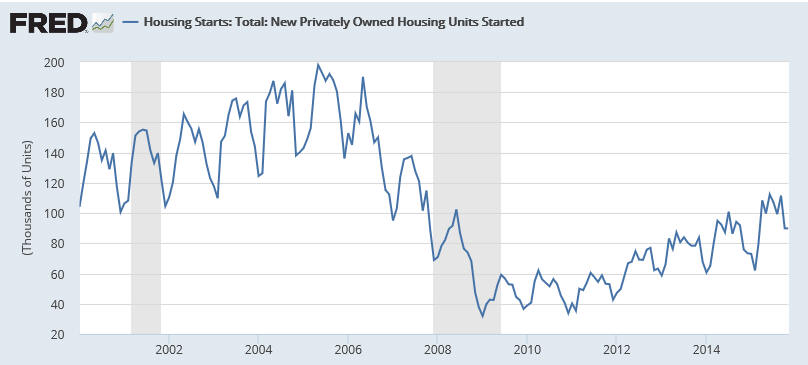

The Housing IndustryWhile the Housing Industry is slowly improving, it is facing significant headwinds. Housing Starts are still way below the levels during the 2005-2006 years. First-time home buyers may have substantial student debt and the increased credit requirements of Dodd-Frank legislation have made mortgages more difficult to obtain. Many millennial have moved back-in with their parents and are delaying the formation of new households. The following graph shows the peaks and valleys of Housing Starts since 2000 and the steady growth since 2010 is apparent but the industry is still struggling.

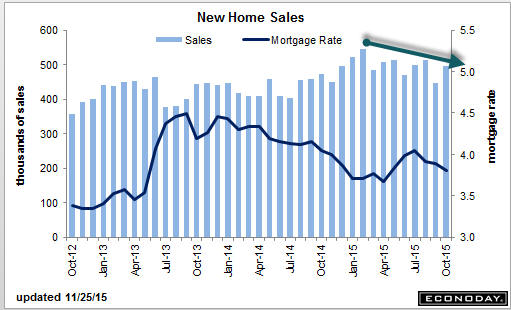

New Home Sales in recent months have not been spectacular and after hitting a high in February 2015 have been slowly declining.

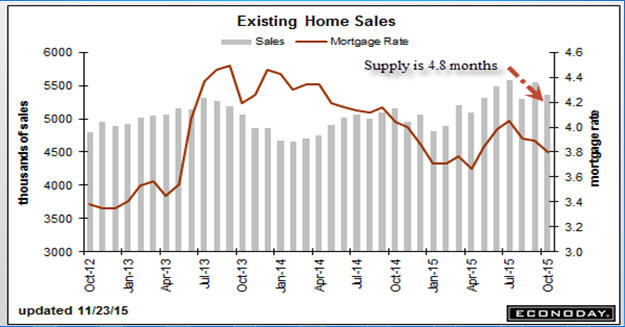

Existing Home Sales appear to have slowed in the last few months.

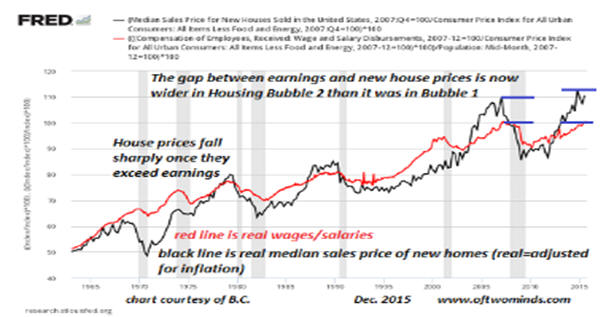

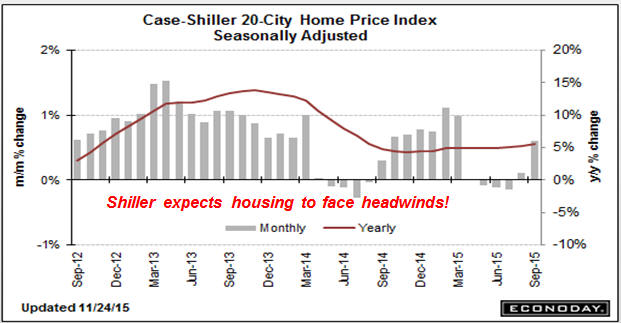

Part of the reason for the slowdown in housing is that housing prices continue to increase. However, in the last Case-Shiller report, Shiller expected that housing would face headwinds going forward as many homes were being priced out of the reach of buyers.

The following chart from oftminds.com points out that the gap between earnings and new house prices is now wider in this housing bubble than it was in the housing bubble of 2008-2009 before the crash.

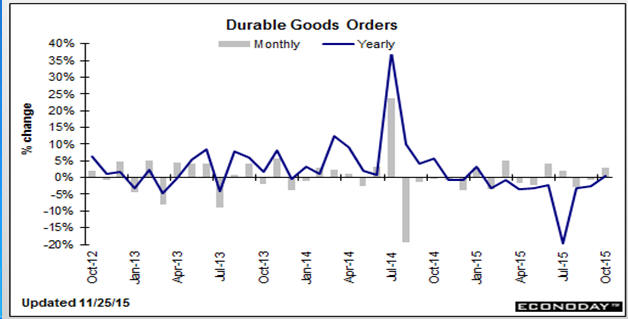

Production and ManufacturingIf housing and the consumer are not going to move the economy forward, does the manufacturing sector have the ability to carry the economy? Of course, exports will be facing a global recession and a dollar that currently is rising as hot money flows towards the U.S. Durable Goods Orders since October 2014 have been barely bouncing along the flat line ... or what John Mauldin might describe as "muddling along."

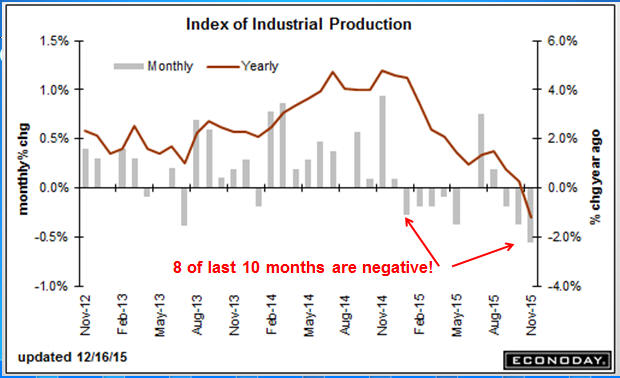

Unfortunately, Industrial Production for 8 of the last 10 months has been negative.

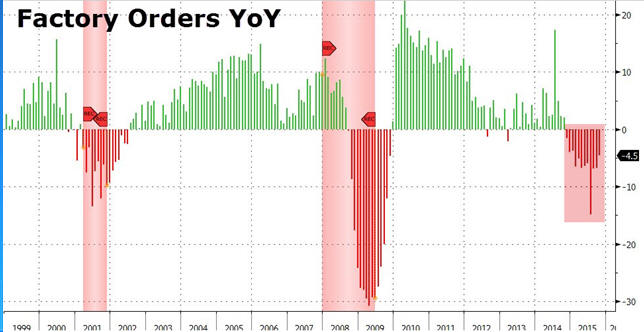

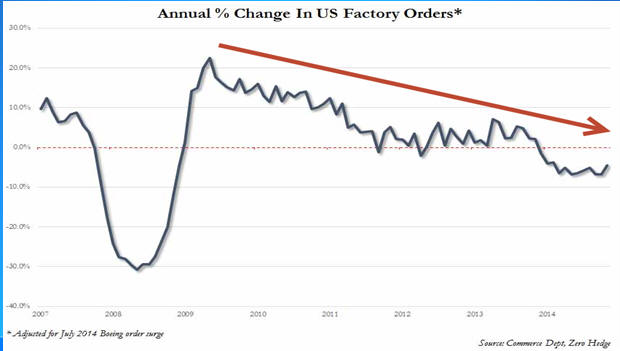

Since late 2009, the annual percentage change in U.S. Factory Orders has been in a downtrend.

In fact, you might even say that Factory Orders on a y/y basis are in a definite recession.

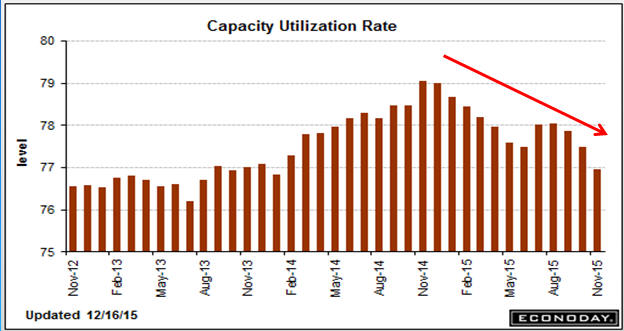

Moreover, the Capacity Utilization Rate continues to fall as shown in the next chart.

If consumers, housing and production are not moving forward, what is the Outlook for growth in 2016. The rest of the world is in a recession and the U.S. could slip into "official recession during 2016."CommoditiesAs noted earlier, the CRB index is at historic lows which suggests that deflation is a larger threat than inflation. Fundamental economists have used the price of Copper as an indicator of forward economic prospects. The following graph of Copper is not encouraging.

Crude Oil is under $35/bbl. and at levels not seen since 2009 and because of low demand and current extraction levels plus the resumption of production by Iran, it could easily move below $30/bbl.

The agricultural sector has been under significant price pressure for the last several years as shown in the next three charts of Wheat, Corn and Soybean Futures.

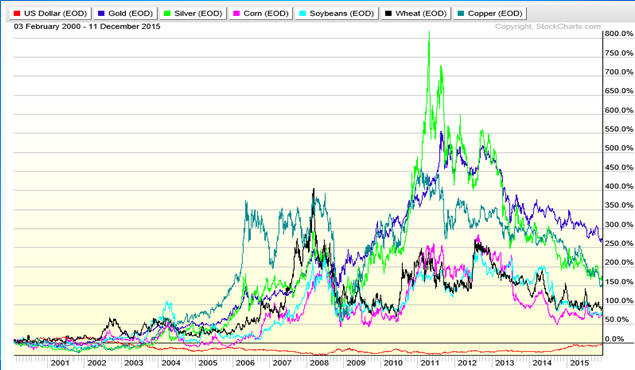

As the above charts illustrate, the Metals, Energy and Agricultural sectors are definitely in contraction and participants in those areas are facing major changes in market conditions, bankruptcies and/or restructuring to survive the current economic conditions facing them. CurrenciesWith the exception of the U.S. Dollar which has benefited from hot money flowing into the country as recession has grown throughout the world and political turmoil roils markets making the U.S. seem like a "safe haven." Both Gold and Silver which historically have benefited from upheavals have found little interest by investors during the past two years as seen in the following charts.

With the exception of the U.S. Dollar and the Chinese renminbi, most other major currencies are under serious pressure. The Chinese renminbi has traded within a tight band with the U.S. dollar in recent years. However, with the addition of the renminbi in the IMF's SDR basket, China has stated that it might loosen the trading band with the U.S. dollar going forward.

The other major trading currencies are showing signs of weakness as seen in the following charts.

Performance of selected currencies and commodities since January 2000 is shown in the following chart. Gold, despite its recent selloff, remains the best performer in the past 15 years.

The Impossible Dream

I trust that as you have read the Outlook 2016, you became aware of some of the problems in the Ministry of Truth's economic data. ConclusionAs we have analyzed the economy, it is obvious that it is, at best, under stress and there is not a single sector that is doing well enough to carry the economy forward. There are many signs that investors ought to be concerned about deflation rather than inflation going forward both in 2016 and beyond. The Baltic Dry Index serves as a proxy for the World Economy. The following graph shows that the world is not doing well and since the U.S. is part of the world economy, it stands to reason that 2016 has a few major problems which politicians and central bankers will be unable to solve despite their rhetoric.

Some of those signs are summarized in the following table:

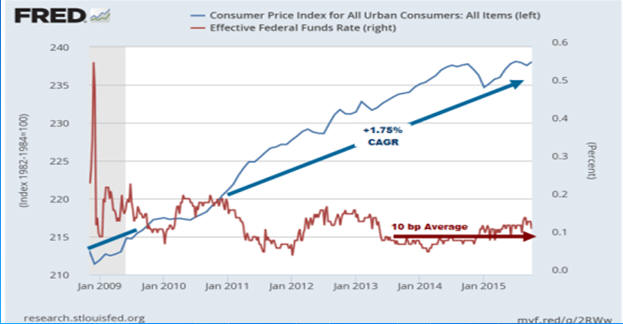

Since January 2009, the artificial interest rate environment provided by the FED has created a major problem even using the MOT's CPI as the gap has widened between the CPI and the Federal Funds Rate as seen in the following graph.

While that gap has enabled the major banks to partially rebuild their capital structures, it has definitely created a major shortfall for the low and medium income classes in the U.S. As the FED interest rates low, many individuals and institutions seeking yield were forced into the emerging bond world and/or the high-yield bond universe. Both of those investment vehicles are now in the melt-down stage with many investors finding that their capital has been seriously damaged.

2016 PredictionsFor what it is worth, here are my predictions for 2016. As the Boy Scout motto goes, "Be Prepared!"

But then .... 'Tis Only My Opinion! Fred Richards www.adrich.com Corruptisima republica plurimae leges. [The more corrupt a republic, the more laws.] -- Tacitus, Annals III 27 'Tis only My Opinion! Archive Menu, click here. This

issue of 'Tis Only My Opinion was copyrighted by Strategic Investing in 2015. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||