'Tis Only My Opinion!

May 2004 - Volume 24, Number 5

![]()

![]()

Why has common sense disappeared? |

|

| Perhaps, you saw the world-wide coverage of the Highland

Park police handcuffing a 97 year-old woman here in Dallas and hauling her

off to jail for failing to pay a ticket for an expired registration.

The police defended the actions of their patrol officer by simply stating

that they were following policy and the instructions of the court which

had issued a bench warrant. The police officers were only obeying

the letter of the law. The court wanted its money and with all taxing agencies facing budget problems, an increase in fines has been factored into many city and county budgets. What troubles me most is the attitude of the police officer in this case who could have taken steps other than those which were chosen to handle this matter. If a law was passed that said that every 80 year-old driver was to be pulled over and shot for driving, would this police officer had followed the "policy and instructions of the court." Unfortunately, based upon the recent example in the last century of Germany, we can not assume that the "policies and instructions of the court" would not be mindlessly followed. Zero-tolerance and political-correctness coupled with the plaintiff's bar have enabled our society to adopt policies and guidelines where those charged with maintaining public safety don't have to use any common sense. It's the law is the only reason. As a result, we see police officers handing out tickets at 3 a.m. at red lights where no traffic is moving after a car has waited five minutes for the light to change. Or we see police using radar guns in school zones, a minute after the school zone becomes active but with not a child in sight as it is a holiday for them. But, of course, the law must be obeyed implicitly. The real crime is that in the drive for revenue (and that is what is really behind most increased traffic stops and not traffic safety), the legal system has forgotten common sense.

|

|

Is the bear market rally over? |

|

|

During the past week, we have seen a rush to exit the stock market particularly in the small and medium cap stocks as fears of inflation and potential interest rate hikes began to appear. Perhaps, investors are beginning to realize that the inflated levels many of these stocks have reached do not justify their valuations. The following chart shows the market action of the small and mid cap since the beginning of 2004.

The graph clearly shows that the peak for each of these indices was in early April and since then, the trend has been downward. The following graph shows the changes in various indices since the first of the year. Obviously with the recent pull-back, there is not much to cheer about despite the recent good earnings reports. Perhaps, the rise in the forward-looking indices expected more or is now expecting lower economic activity in the months ahead.

In any event, when the Investor's Business Daily suggests that "cash is for the prudent investor" the rash of distribution days in the last three weeks should finally put the finish to the market rally that began in March 2003. O'Neil felt for some time that we were seeing a new bull whereas my readers know that I have always considered this rally to be just rally in a secular bear market which could last for many years.

|

|

The Outlook for the Economy |

|

Outside of a few economists and stock market analysts, I have a sense that many of today's investors and professional money managers really don't have a clue. Mark Cuban in his forward to Alex Berenson's book, "The Number," makes the point succinctly and powerfully. If you want to get better insight into the action of the lemmings in today's market, be sure to read both the forward and the book. It doesn't get much clearer than this. The nation's GDP was reported this week as increasing 4.2% for the 1st quarter of 2004 while the deflator increased to 2.5% indicating inflation was being injected at a higher rate into the system.

Bill King who writes The King Report is one of the best analytical minds around. On Friday, April 30th, he had a few observations about the GDP numbers which are pertinent:

On May 4th, the Fed will meet again to consider the outlook for the economy and to issue a communiqué. Very few expect that the Fed will increase interest rates at this meeting. In an election year, many pundits believe that the Fed will accommodate the administration by running the printing presses while keeping interest rates low. However, the course of action adopted by the Fed has re-inflated the housing bubble which has been a major force in keeping the economy moving ahead during the past three years. Although new home sales and existing home sales have continued to grow, some of the recent growth is probably because of interest rate fears.

During the past week, new mortgage applications rose about 7% while the refinancing index declined as interest rates have continued to move upward. With building permits increasing and rules for mortgages beginning to tighten, the building industry's all-time record "for-sale" inventory may be headed for trouble. Prices of new homes continue to increase as builders attempt to pass on increased costs throughout the construction process. In the last few months, we have seen major shortages of things like nails develop which further restricts the building cycle. Consumer confidence recovered somewhat during the latest reporting period as shown below. One of the major factors influencing consumer confidence levels is the job market. Perhaps, this was in reaction to the recent job report which showed that some 380,000 jobs had been added . . . although on closer inspection, we find that most of those jobs were part-time ones at low wages. But headlines are read by the populace.

The chart also shows a decline in retail sales for March which is also being carried over into April. When you realize that these numbers are not adjusted for inflation, the actual amount of goods being pushed out of the system has fallen. It will be interesting to see the industrial production and inventory numbers as they become available. The employment cost index was reported this week and a major portion of the increase in this index was caused by increased benefit costs. The downward pressure on wages and salaries which started in the second quarter of 2000 continues to put wage-earners further into a box. When wages begin to increase, we will really know that we have started to come out of the economic malaise.

For months, critics of the administration have pointed the jobless recovery as evidence of Bush's inability to get the economy on track. Of course, Bush really has very little to do with the economy but like others before sits in the hot seat. Unemployment continues to be a problem although new jobless claims have fallen from the peak in the 3rd quarter of 2001. Unexpectedly, the help wanted index fell during March which is based upon newspaper column-inches. Maybe, the role of the internet in finding jobs is making this index less reliable.

Congress extended unemployment benefits but we are now seeing many laid-off workers finding themselves losing those checks. One economist suggested that was probably the reason we had so many part-time new jobs added to the labor force last month. The real problem with these statistics is that they are continually revised upward . . . seems that the green-shade statisticians in the BLS can't add numbers correctly the first time. Nevertheless, a glance at the above chart shows that new jobless claims have been gradually diminishing since the 3rd quarter of 2001. Disposable income on a monthly basis continued to fall during March as shown below. Growth in this statistic has best modest since October 2003.

The low rate of increase in disposable income has also impacted consumption expenditures since the year-end as shown in the following chart.

If consumers continue to reduce the rate of consumption purchases, it will have a negative impact on the economy. Easy Al and his cohorts have the money spigot turned wide-open and we still have an economy which is not growing at a rate that most would like to see. As a result, the University of Michigan consumer sentiment index also showed a slight decline for the month of April.

The NAPM index was released for April and showed a significant jump following March's decline.

So the best that can be said is that earnings for the 1st quarter appear better than many expected. The economy is still not producing many full-time, high-paying jobs. Unemployment benefits for many laid-off workers are exhausted. As a result, the markets have been worried about the course of interest rates and have pulled back off their recent highs.

|

|

Will the Federal Reserve increase rates in May? |

|

|

In my opinion, the smart move would be to increase rates by 50 basis points in May and then wait until after the election. This would signal to foreigners that they can expect further increases next year and that we are serious about defending the dollar. Of course, unless Easy Al announces his retirement in June, that will probably not happen. However, we currently have a yield curve that resembles the proverbial hockey stick and with a spread that is about twice what the historical spread from short to long has been. Historically, we have seen a spread of between 200 and 250 basis point in the yield curve. Currently, we are over 410 basis points and the spread has been increasing during the past two weeks as shown in this chart.

The following chart of the 30 year bond clearly demonstrates that the pressure on rates has been steadily moving upward. The long-bond was the first to penetrate the long-term downward trend line.

During the past two weeks, the ten year bond has also pierced the long-term trend line increasing the spread between the fed funds rate and longer-term issues.

With both the 10 and 30 year yields now above the down-ward trend lines, the prudent move for the Fed would be to decrease the spread. However, since this is an election year and jobs have not recovered, the Fed will probably wait until the end of June or August. As a result, the dollar will probably continue to fall in the channel which it has occupied since the January 2002 peak.

The Fed can only continue to devalue the currency to pay-off the horrendous trade and budget deficits which the U.S. continues to pile up. As a result, the money supply will continue to surge and the dollar will continue to fall.

|

|

How bad is the trade deficit? |

|

|

The U.S. trade deficit continues to run in excess of $40 Billion each month. For the year, the trade deficit will probably set a new all-time record. There are those who suggest that this is just "vendor-financing" and our citizens should not worry. Of course, we are also only paying for it with worthless paper and not "gold or silver." Nevertheless, it represents a major transfer of wealth. Only by refusing to pay or by inflating the value of that paper like Germany did in the 1920's hyper-inflation do the holders really lose. Japan, China and the other countries which are flooding the U.S. with goods in exchange for paper are only providing jobs for their citizens. At some point, the value of the paper which they receive in exchange for those hard goods will become of great concern. However, at the moment, China is gambling that they can prevent a revolution by decreasing the unemployment rate. However, the growth rate of China has now become of major concern and is forcing up the prices of commodities world-wide and creating shortages of raw materials as well as transportation vessels. Just let a little hint that the Bank of China may slow down the growth by increasing lending standards and what happens? The commodity markets head south. The Fed is thus in a major bind trying to walk the tight-rope of expectations while keeping foreign investors hoping that there will be some value in the notes and currency which they hold. |

|

Looking without rosy glasses at the federal deficit? |

|

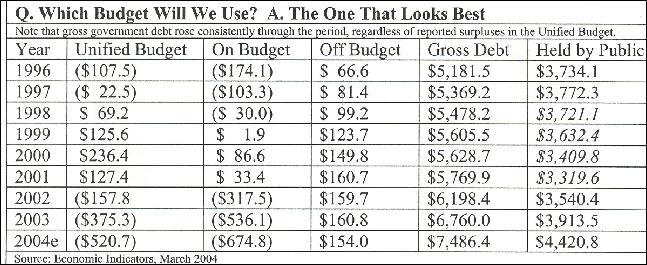

The official unified budget of the U.S. for FY 2004 issued last year suggested an all-time record deficit of $520.7 billion which will cause another increase in the debt limit to perhaps $8 trillion. Now that would not be so bad if we used real accounting to measure the budget rather than smoke and mirrors accounting. However, with the increased cost for the Iraq war and the prescription drug benefit, who knows how high the deficit will be.

As this table points out, despite the unified budget showing a surplus, the gross debt owed by the United States government continued to increase in every year. On a realistic basis, there are estimates that the federal deficit without borrowings from social security and other trust funds could exceed $750 billion in fiscal 2004. |

|

Watching the value of their paper become worthless. |

|

As the U.S. government continues to build up massive deficits in trade and government spending, foreign holders of our debt are becoming less inclined to purchase more debt at the interest rates currently being offered. As a result, interest rates are slowly being forced upwards. Foreign holders of debt have already seen about a 25% loss in the value of their holdings as the value of the dollar has fallen since January 2002. It take quite a few years of interest at 4% to get one's capital back. For a lesson in vendor financing risks, one should ask the telecom manufacturers who provided all the fiber-optic equipment. Most of those involved in the vendor financing scheme have fallen upon hard-times or disappeared from the scene entirely. |

|

Generational accounting suggests that the U.S. is already bankrupt. |

|

|

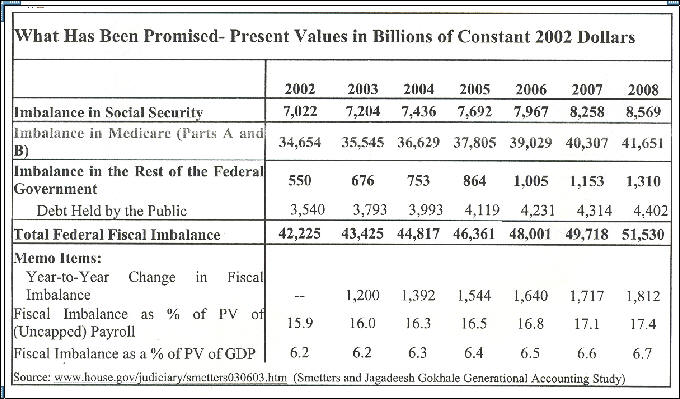

Politicians have promised way more than the current tax structure can deliver in social security benefits, prescription drug benefits, and other give-away programs to win votes.

As the above table shows based upon generational accounting, the U.S. has a present value liability of about $42.2 billion. If you add up all the assets in the U.S., you only get a total net worth of about the same amount. Hence, the country is essentially bankrupt. Unless steps are taken by the politicians to either raise taxes, reduce future benefits, and cut spending, the fiscal imbalance continues to grow. Another study by Texas A&M suggests that the fiscal imbalance may actually be over $70 billion . . . but then we all know about the accuracy and competency of those Aggies. By continuing to flood the market with money at low interest rates, the value of our dollars will continue to weaken further increasing the fiscal imbalance. |

|

Will the Fed act to save the dollar? |

|

| The Fed has painted itself into a corner and probably does

not have the courage to attempt to save the dollar. About the only

way is to increase interest rates and Easy Al probably does not have the

political will to do so. In his recent speeches he has ignored the

problem caused by a rising money supply and the increasing difficulty of

funding the federal debt issues. During the past three months, the

Fed has had to purchase an increasing percentage of the U.S. Treasury

offerings. The Bank of Japan has suggested that its continued support of the yen/dollar relationship is under serious review and that they might begin diversifying their foreign reserves from dollars to other asset classes. With the Malaysian dollar already making inroads into the Middle Eastern trade settlements and Euro's becoming more acceptable in international trade daily, continued low interest rates will not help maintain the dollar as the world's reserve currency. That role as the world's reserve currency has been held since Bretton Woods after WWII and has enabled the U.S. to dominate world affairs. The loss of that role could be a serious blow to the U.S. as a world power. Yet, I doubt if the Fed will increase rates until after the election and hence, Bill Bonner may well be correct when he suggested that the U.S. trade-weighted dollar currently about 92 will be at 40 by the end of 2005. |

|

Conclusion |

|

Except by inflating away the deficits and depreciating further the dollar can the Fed prevent a fiscal collapse. The odds of being successful are stacked against them. The ability of the U.S. economy to continue to grow is going to be hampered by the lack of fiscal restraint by the Congress as well as the reluctance of the Fed to take the tough steps to put this economy into a major recession under which the excesses caused by the infusion of the flood of easy credit and liquidity can be worked down. The real question is whether the threat of our military superiority will prevent China and Japan as well as the Euro nations from initiating a dollar run in an effort to bankrupt the U.S. David Cassidy of the Lipper organization recently suggested that the probability of a run against the dollar in the next few months was at least 10%. Peter Eliades, a well known technical analyst, recently declared that there was "nothing" holding up this market. The action of the past few days bears that opinion out. Even our friend, William O'Neil, is now suggesting that "cash is where the prudent money should be." Hopefully, that will be my stance. Remember KISS and SF. Keep it safe, simple and stay focused. Safety should be uppermost in ones thinking in today's environment. |

|

But then - 'Tis Only My Opinion! |

|

| Fred Richards May 2004 Corruptisima republica plurimae leges. [The more corrupt a republic, the more laws.] -- Tacitus, Annals III 27

This issue of 'Tis Only My Opinion was

copyrighted by Adrich Corporation in 2004.

Last updated - July 6, 2008

|

|