'Tis Only My Opinion!

February 2004 - Volume 24, Number 2

![]()

![]()

The US dollar is in trouble as the world's reserve currency! |

|

|

Many U.S. investors focus upon the level of the equity markets to determine the performance of their portfolios on a relative basis. Unfortunately, they are generally ignoring the fluctuations of their currency versus other currencies when they make that comparison. Since the Bretton Woods agreement, the U.S. dollar has become the world's reserve currency and as such it was not subject to many of the restraints other fiat currencies faced. Today, many measures suggest that over one-half of all American currency is held overseas. Also, close to half of all U.S. debt including state, local and federal debt and corporate and consumer debt instruments are held by foreign interests. As the trade deficit and the federal budget deficits have continued to increase since the 1980's, there has grown an increasing reluctance upon the part of foreign investors to subsidize our spending binge. Also, for political reasons associated with the dominant military position of the U.S., many politicians around the world believe that it is easier to negotiate with the U.S. using financial leverage rather than through possible military solutions. For half-a-century, the U.S. has been able to buy merchandise from its trading partners and to issue fiat currency in exchange. However, the value of that currency is based upon nothing than faith. Recently, we have seen a significant deterioration in the value of that currency. The spread between U.S. interest rates and almost all other nations other than Japan has continued to increase and now stands near all-time records. The dollar's decline coupled with low interest rates has seriously eroded the risk/reward advantage which U.S. financial assets have long enjoyed. Other than China, most major powers including Russia and the European nations understand that the U.S. military advantage is a formidable one. As a result, the current role of the dollar as the world's reserve currency is under attack as finance ministers seek to find a way to protect their countries financial position.

|

|

Two little words generate a stampede |

|||||||||||

The latest Fed communiqué changed the language about interest rates from "reasonable period" to "patience." Almost immediately, many hedge funds and investors tried to dump their holdings causing stock prices to fall dramatically in a very few minutes.

The DJIA dropped 200 points in about 90 minutes as bids became scarce. In this day of black box trading, it would be interesting to see how much of this decline was generated by computers rather than investors.

If the possibility of an interest rate hike sometime in the unknown future

time-frame can spook the hedge funds like Wednesday afternoon did,

investors should become extremely cautious about the effect of either

actual hikes or an unexpected event like a terrorist attack or a major

change in policy by politicians seeking political advantage.

A close look at the FOMC statement would also suggest that the word change

from "reasonable period" to "patience" does not suggest that the Fed will

raise interest rates in the near term. Rather I believe that it was

simply a ploy to use at the G-7 meeting next week. The G7 finance ministers - from

U.S., Japan, Germany, France, Britain, Italy and Canada - last met in

Dubai on Sept 20, 2003. The key passage of their communiqué said: The U.S. dollar index peaked in January 2002 at the 121 level. The following chart shows the price movement on a weekly basis since January 2000.

Fiat currencies like the U.S. dollar trade largely on the basis of the risk/reward perception between countries. A close look at this chart shows that beginning in January 2002, the dollar index has been falling dramatically against most foreign currencies including the yen and the Euro. Only the Chinese renminbi has remained equal to the U.S. dollar as they have linked their currency to the U.S. dollar. That linkage has enabled the Chinese to sell their products cheaply and increase their penetration of U.S. markets while building up their currency reserves. Since the last G7 meeting in Dubai, the daily price action of the index is shown in the following chart.

Since the Dubai meeting, the dollar has fallen:

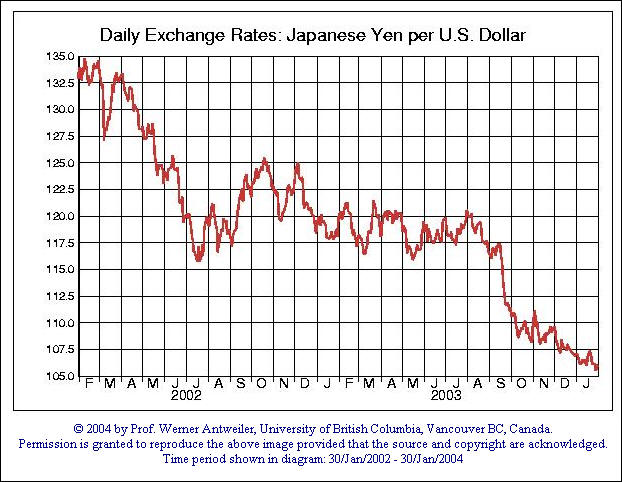

Clearly, this decline has created major dislocations in the currency markets. At the moment, the full extent of this problem is hidden as many American corporation operate on an international basis and can benefit from the falling dollar when repatriating dollars to the U.S. The effect upon our CPI and PPI will generally take from six to nine months to show up. The Japanese economy is stagnant and their export business is beginning to expand slightly. However, with its two major export markets (U.S. & China) tied to the U.S. dollar, the Japanese Ministry of Finance has been spending vast sums to defend the yen against rising against the dollar. During 2003, the official figures show that the Japanese spent $168 Billion in currency interventions and during January 2004, they spent another $68 billion trying to keep the yen from falling below 106. At the end, they were unsuccessful. The unanswered question is how low would the dollar have gone if the Japanese central bank had not provided that support. Although the Bank of Canada reduced its interest rate in January and served notice that it might do so again in the near future, other central banks have not followed their lead. In fact, it would appear that the spread between the current U.S. interest rate level and foreign interests rate have become great enough that it is beginning to change the historic pattern of risk/reward investing followed by many large investors. When the interest rate spread is also linked to the U.S. dollars slide since January 2002, almost every foreign investor has lost not only the difference in interest rates as well as a significant loss on the value of the investment. This is a situation that will not continue. The G7 meeting will be held in Florida this week. It is doubtful that the meeting will have a significant effect upon the downward trend of the U.S. dollar. The Fed's announcement that interest rates may increase in the future should not worry investors at this time. The U.S. economy is not increasing jobs at the 200,000 jobs/month clip that might move the Fed to act. Besides it is an election year and the Fed always tries to accommodate the President by not raising interest rates until after the election.

|

|||||||||||

Interest Rates and the Fed |

|||||||||||

With the trade deficit running in excess of $450 billion in 2004 and perhaps, $550 billion, foreign investors are now facing a need for the U.S. Treasury to also finance an additional $544 billion in fiscal 2004. With interest rates remaining at near record low levels, the U.S. Treasury continues to borrow at the short end of the yield curve. In March 2000, the yield curve looked as follows with long-term yields in the 6% range:

With 10 and 30 year yields between 4.5% & 5%, prudent long-term Treasury Secretary's should be trying to move the average maturity curve towards the long-end. Because of the size of the debt, however, any increase in overall interest rates can further add to the budget deficit. The Fed's rate cuts since 2000 have driven down the yield curve on the short end of the curve dramatically but the long end has been more difficult. Selected interest rates since 2002 are shown in the following chart.

Note the increasing spread between the short-term interest rate beginning in April 2001 and long-term rates. This divergence suggests to me that the Fed is unable to move long-term rates with changes in the short-term rate structure. The current yield curve is shown below:

With Congress refusing to control spending and the U.S. Treasury not taking advantage of historic low long-term interest rates, when crunch time goes, the U.S. taxpayer will find themselves facing much larger interest rate costs in the future.

|

|||||||||||

Changes in the Ownership of U.S. Treasury Debt |

|||||||

|

Since 1991, the federal debt has almost doubled and with the current projected deficit of $544 billion for fiscal 2004, the strain of financing that debt with low interest is beginning to be seen in the marketplace. During the past decade the ownership of the U.S. Treasury debt has shifted as shown in the following chart.

Clearly, private U.S. ownership has declined since the peak in 1995. During that period, foreign holders of our debt have grown substantially. However, the chart also shows that during the period, the largest purchaser of our federal debt has been the U.S. Government trust funds and the Federal Reserve.

|

|||||||

Percentage of U.S. Treasury Debt owned by foreign interests |

|||||||

|

For many years, the percentage of U.S. Treasury Debt owned by foreign interests has been increasing and has doubled since 1986 as shown in the following chart. The latest figures from the Federal Reserve put the current figure at about 44%.

|

|||||||

When will the rubber hit the road? |

|||||||

|

The major financial risk facing the fiat currency system is the point at which one or two creditor nations decide to no longer provide "vendor financing" to the U.S. and either cease buying additional debt or begin to significantly reduce their holdings of U.S. dollar denominated reserves. The largest holder of U.S. external debt is Japan with about $680 billion worth of Treasury paper as of 12-31-2003. Last year, Japan supported the yen/dollar relationship to the tune of $168 billion. In their fiscal 2004 budget, the Japanese indicated that they might support the yen/dollar relationship by up to another $330 billion. In January 2004, the official Japanese figures show them spending $68 billion in their currency manipulation efforts to keep the yen/dollar relationship above 106. Yet, despite the massive amounts spent, they were not successful. As a result, trial balloons have been floated suggesting that "enough is enough." Alternatives such as restructuring a significant portion of the currency reserves into the Euro or gold have been floated. The assistant Minister of Finance even suggested that Japan might increase its gold currency reserves from 1.6% to 10% over the near term. Of course, a change of this magnitude would require two years of current gold production. But as noted above, buying dollars to support the yen has been a losing proposition for the Japanese during the past three years as the dollar has depreciated.

The European Central Bank indicated this past week that it has no reason to intervene further in the currency markets in an attempt to reduce the Euros value against the dollar. |

|||||||

The $544 billion budget deficit for Fiscal 2004 |

|||||||

The federal budget deficit was just raised for fiscal 2004 from $480B to $544 B last week and that is before the revised costs for the new Medicare package has been added. The President's Budget office suggested that costs of the new Medicare package passed by Congress were understated by at least 33%. Oops!

As the above chart shows clearly, the real problem with the federal budget is not defense but the continued rapid increase in the cost of social programs. Of course, these are the programs that entrenched politicians use to bribe the voters to keep them in power. Social security and Medicare/Medicaid programs are just one of the many programs that have spiraled out of control since 1950. The drug benefit program recently enacted will probably see the same result. The demographics of the Baby Boomer generation and beyond paint a dismal prospect for the federal budget in the next 20 years. By some estimates, by 2020, the number of people on social security or not working and received some form of welfare assistance will be twice the number of people working. That is a recipe for disaster for these social programs. The current national debt stands about $7 trillion. The cost of a 1% rise in the average interest rate on that debt is about $70 Billion per year. If the Fed were to ratchet up the interest rate to the 4% level in order to slow down the decline in the dollar, the potential added interest would be about $140 Billion per year or about a 25% increase in the federal deficit.

|

|||||||

The IMF becomes suspicious of the U.S. financial structure |

|||||||

|

The International Monetary Fund (IMF) and its sister organizations, the World Bank group, were formed after World War II. The rationale for these organizations was to help faltering countries return to stability and to promote world trade. The IMF agenda is to work for global prosperity by promoting the balanced expansion of world trade through

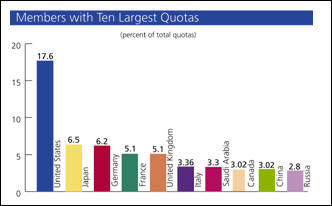

The United States provides about 40% of the funding for the IMF. Since its inception, the IMF has attempted to work with countries that become financially unstable and assist them in restructuring their debts. Since its inception the U.S. has provided about 45% of the total funding for the IMF. Funding quotas are loosely based upon the relative importance of each economy to the total world economy and are revised periodically. The most recent revision occurred in 1998 and since then, the U.S. has a 17.6% quota. The ten largest contributors to the IMF are shown in the following chart.

In almost every case with the exception of the Mexican loans in the 1990's, the solutions proposed by the IMF have not solved the problem. As control of the IMF and its bureaucracy has moved towards Europe and the socialist countries, the ability of the IMF to solve problems has diminished. In January 2002, Argentina defaulted on somewhere between $80 and $100 Billion in sovereign and corporation debt when it cut the linkage with the American dollar. Despite a few additional handouts and rollovers from the IMF and private creditors, Argentina is now proposing to pay eight cents on the dollar some 20 years in the future. Negotiations are at a impasse between the IMF and the Argentine government. The Argentina government is playing hardball. If it succeeds in forcing the IMF and other multinational organizations to write-off 90% or more of their outstanding debt and is able to revamp its economy through alliances with China, India and other developing nations, other nations may soon tell the IMF and its cohorts to take their money and repayment plans elsewhere. If Argentina fails, it may well find itself in the company of Zimbabwe and cut off from the international financial community. One of the sticking points in these negotiations is Argentina forgiveness of some $20 Billion in debts to Cuba at the same time it owes between $80 and $100 Billion to its creditors. Recently, the IMF issued a report critical of the U.S. trade and federal budget deficits. Excerpts are quoted herewith.

The Bush Administration called the IMF's report alarmist. While that may be, often the perception of a problem becomes the reality and foreign governments and investors are now being told by the IMF that the risk/reward ratio for investing in the U.S. is increasing. If the past is any indication, the amount of time for the U.S. to get its financial house in order by either raising taxes and/or cutting spending to balance the budget has been shortened considerably by the publication of this report on January 8th.

|

|||||||

Can the U.S. stem the flight from the dollar? |

|

|

Based upon the spending policies of our state, local and federal governments and the clamor of our citizens for more benefits without being willing to pay for those benefits, it is highly doubtful. The Fed and Congress is faced with a major dilemma. If the Fed raises interest rates to reduce the spread between U.S. rates and foreign interest rates, the federal budget deficit widens and the fragile economic recovery is possibly derailed. If Congress raises taxes in an election year, the Democratic party may well regain control of the White House and Congress. The Fed's current policy of continuing to pump money into the system will probably continue and the administration is hoping that by using hedonic, seasonal and various other tricks, it can fool the citizenry that inflation remains almost non-existent. Massive currency intervention by the Japanese, the European Central Bank and the U.S. might prevent the dollar from falling dramatically in the next few months. But as stated earlier, Japan and Europe are reluctant to continue their support of the dollar. During the last six months, we have seen substantial purchases of physical gold by Russia, China, and the Middle East as well as the traditional markets like India and the Far East. The sellers have generally been the Central Banks. However, some of those sales like Norway, Italy and Portugal were really swaps or the carry trade that were finally reported as sales. The physical gold had entered the market much earlier. Although many nations report holdings of gold, the veracity of those reports is questionable. The U.S. gold stocks were last audited under President Eisenhower in 1952. The extensive work of GATA and the Blanchard lawsuit suggests that almost half of the reported central bank holdings are no longer physically held by the various central banks. Fiat currencies as mentioned previously are subject to subjective perceptions as to value. At the moment, the perception of the American dollar as a safe refuge for capital is shaky. As a result, we are likely to see a further decline in the value of the dollar.

|

|

Conclusion |

|

|

There are many chinks in the armor of the U.S. dollar's role as the world's reserve currency. Last week, the Wall Street Journal actually had an article about using gold as backing for the U.S. dollar again. During the next few years, if we don't experience a financial meltdown, we will probably see other financial mediums like the yen or the Euro as well as commodities like oil, gold and/or silver share the U.S. dollar's role as a reserve currency. The end result will be that the U.S. will be required to become more financially responsible and despite its military advantage, its economic advantage will be reduced resulting in a lowered standard of living in the future.

|

|

But then - 'Tis Only My Opinion! |

|

| Fred Richards February 2004 Corruptisima republica plurimae leges. [The more corrupt a republic, the more laws.] -- Tacitus, Annals III 27

This issue of 'Tis Only My Opinion was

copyrighted by Adrich Corporation in 2004.

Last updated - July 6, 2008

|

|