Is the market action just consolidation or is something else going on? |

|

During the past few weeks, the market internals seem to be suggesting that the rally which began in March is starting to falter. Perhaps, the clearest indication of that can be seen from the plummeting number of the "A" rated stocks in the Investor's Business Daily's Accumulate/Distribution rating as shown below.

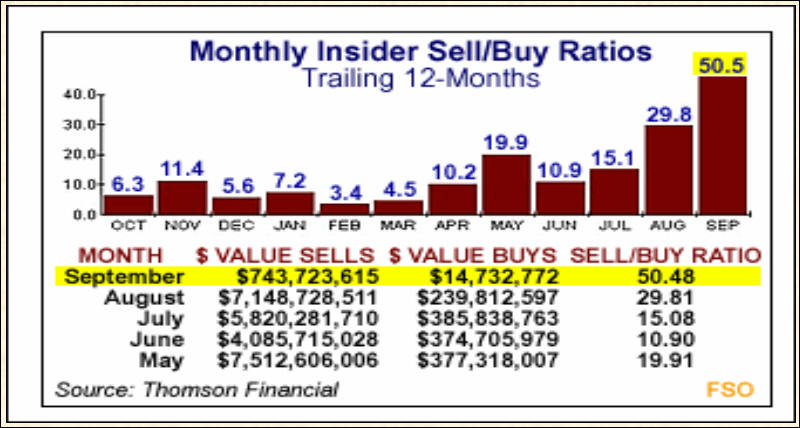

Since June 17th, the Accumulate/Distribution ratings have been dropping. Last week recorded the largest drop in several months of the number of "A" rated stocks. The chart is posted through Friday, September 26. Also, the ratio of insider sales to insider purchases of stocks has risen sharply.

Further, corporate profits in the second quarter were not as robust as initially projected. In fact, corporate profits were down slightly from the 1st Quarter as shown in the graph. Also, corporate profits remain significantly below the levels reached in the late 90's yet valuations on a P/E basis have not fallen to reflect the decrease.

As the saying goes, hope springs eternal and the market loves fools.

|

|

Dr. Richebacher suggests that the recovery is a bureaucrat's smokescreen. |

|

The economic elite declared the last recession over as of November 2001. It was a short recession according to them. Dr. Richebacher, a German economist from the Austrian school, points out that in every one of the previous seven recoveries, jobs have increased. The fact that jobs have not increased in this recovery suggests to him that either the recession has not ended as the elite believe, or something much more serious is happening to our economy. I shall let the good doctor speak . . .

The entire article by Dr. Richebacher can be found at:

The past 22 weekly reports from the federal government on the new jobless claims have been revised upward the following week. If I were a cynic, I might believe that they were doing it on purpose. Of course, that allows the current week statistics to not look so terrible.

|

|

Is the Technology sector going to improve? |

|

|

During the past quarter, there has been a lot of hope that the technology sector was recovering. Certainly, the Nasdaq 100 stocks were leading the market rebound. However, it now is apparent that the recovery is not as robust as perhaps was forecast just a few weeks ago. SUNW just announced that sales were slow and that it was going to take a $1 billion charge against net worth. Now we are somewhat blasé about a billion dollar write-off given the bankruptcies and write-downs of the past two or three years. But a billion dollars is still a lot of money. In the last two weeks, we have had conversations with many technology executives about sales and earnings prospects for the coming quarter. While they remained hopeful on balance, we did note that several indicated that incoming orders had slowed down since September 15th. We are now looking for Christmas sales and shipments to be in the manufacturing pipeline. Motorola's new mobile phones won't be ready on time and the CEO suddenly found the keys to the executive washroom did not work. Of course, it was not his fault but he got the axe. Today, I visited an old friend who handles corporate relocations in the Texas area. His comment was his business had dried up within the last week whereas it had been gradually increasing during the past 120 days. He also said that he could get all the moving vans he needed immediately by just placing a phone call. The COMDEX flyer for the big show in Las Vegas arrived last week. I've only missed one show due to illness since it started. The number of exhibitors who will be there may be the lowest in COMDEX's history. There should be a lot of hotel rooms available. This past week, Nanotech research got a $25 million grant from the U.S. government. Based upon the amount of hype, the recipients at UTA, UTD, Rice and the Air Force put out, you would have thought that nanotech was just around the corner. Well, I am here to tell you that nanotech is a few years off from being a highly successful commercial venture. Heck, look at the venture capital funding amounts that have gone into nanotech the last year. Better have a microscope as it is only a pittance of the billion SUNW is writing off. So that leaves bio-technology. Again, research continues but substantial sales and impact to the U.S. GDP is probably a few years away also. Boeing is about ready to close its 757 production line. Intel is introducing higher speed CPU's but the real constraint to most computers is not the CPU but the input/output devices necessary to handle the throughput. Storage continues to grow and become denser but then when you lose a storage device, you better have a complete backup. Microsoft will introduce its new Office Suite in October. Will it be a runaway sales hit, or will the public see it as just another minor improvement that will require lots of learning and upgrade time to continue to do the same tasks currently performed by Office 2002, or earlier versions.

|

|

We've started fall harvest and the crops don't look good. |

|

On Thursday, September 25th, the combines began rolling on farms in North Central Iowa. Last year, we averaged over 58 bushels of soybeans per acre in North Central Iowa. This year, we are finding soybean yields in the 30 and 40 bushel range. Look for soybean prices to improve. There were two major problems accounting for this production decline. First, August was the driest month in history in Iowa. Second, the infestation of Chinese aphids (an insect) became a serious threat. However, initial yield data is inconclusive about whether spraying for the pest was economic. The other major crop, corn, was also affected by the drought conditions. However, the ground moisture was sufficient to allow the corn to feed through its roots for a longer period of time. However, the corn ears did not fill out completely and I'd expect that crop yields will be below trend-line this year.

|

|

Are foreigners beginning to bail out of the U.S. Dollar? |

|

| The Dubai G-7 meeting set the FOREX market quivering.

One of the immediate results was the U.S. dollar beginning to weaken.

The following chart shows the slide of the U.S. dollar index which has

been falling since it peaked in January 2002.

On September 30, the dollar closed at 92.75, less than .90 above the previous low. If the dollar takes out that level, the next support line is in the lower 80's. If you look at the downward slope of the dollar's fall since the end of August, you have to be concerned at the gradient. While there is a gap below 95 that might have to be filled, the pressure remains to the downside. The Japanese have admitted to spending over $40 billion to keep the yen from appreciating too much in September. Yet the yen rose from 118 to 110 against the dollar. The Euro also was strong against the sagging dollar. If the trend continues below the 91.88 level, you can expect carnage in many foreigner's portfolios. U.S. corporations with overseas operations will benefit from the slide when they repatriate earnings. However, so far, the decline in the dollar from the 120 level in January 2001 to now has failed to improve export sales of manufactured goods from the U.S. Of course, the major reason for that is we don't manufacture much anymore.

|

|

The Money Spigot is full open. |

|

| The Fed continues to keep the money pump running.

Greenspan and three other Fed governors in speeches recently have stated that the policy of the U.S. Treasury and the Fed is to debase the U.S. currency. That reminds me of the "Fall of the Roman Empire" with which I became familiar during my years of Latin. The Fed's policy is to "Inflate or Die!" Unfortunately, it could easily turn into something much worse . . . "Inflate and Die!" as the German hyper-inflation scenario proved. Can it happen? Who knows. However, prudent investors have to understand the difference between currency and wealth. The major difference is that wealth can endure if it is situated in the right type of assets. Currency, on the other hand, may only have use as toilet-paper. We also must learn to decipher the spin contained in corporate and governmental statistics. What one reads in the headlines is quite often significantly different from the underlying facts. As an Presidential election is now only 13 months away, you can be sure that efforts will be made to keep the ship afloat. There is some question in my mind that the party will continue until then. As a result, prudent investors need to be aware of the vagaries of fiat money. Gold and the un-hedged gold index ($HUI) have made substantial gains in the last three years . . . but if you listen to the mainline press, you would not know it. The following chart of gold could be just the beginning of gold's move.

Gold has now taken out the February high of 388.90 and the next resistance point is about 420. If it breaches the 420 level, it could go much higher. We are seeing major changes taking place in the gold market. Production is falling, producers are closing out their hedges, China has opened gold ownership to their citizens for the 1st time in 70 years, China has also stated that they will be reducing their U.S. dollar reserves and moving into gold and Euro's, Argentina is going to back their currency with gold, the Islamic countries will be using gold dinars to facilitate international trade between them rather than U.S. dollars, and several oil producing countries are beginning to seek settlement of oil shipments in either gold and/or Euro's outside of the Islamic countries. Further, the SEC is about ready to approve a Gold ETF for sale. To me, all this activity points to a fundamental shift away from fiat currencies like the U.S. dollar as a storehouse of wealth. At today's low interest rates, the cost of holding gold versus the potential interest and currency devaluation loss from holding U.S. Treasuries by foreigners is a "no-brainer decision."

|

|

Conclusion |

|

| We live in interesting times. Those that don't

remember the lessons of history as bound to repeat them. Today, I was

privileged to hear a Dallas native, Dallas Cothrum, a tenured history professor

in the University of Texas system discuss the Civil War and other subjects. History in the liberal academic environment has become not only revisionist but the lessons of history are so sugar-coated that one wonders if the history professors will continue to write our history books. According to this professor, useful history during the next hundred years will only be written by those outside the academic environment. The capitalist system remains a "boom and bust" cyclical system. However, failure to wash out the excesses when they occur always ends up being more costly in the end. Politicians, and particularly, incumbent politicians are willing to sacrifice the economy for re-election. Today, we are trying to prevent the cycles from occurring. With the huge capital account and trade deficits, state, local and federal deficits headed to the stratosphere, the day of reckoning is not too far off. It behooves investors to be prudent, protect their assets and stay out of the limelight.

|

|

But then - 'Tis Only My Opinion! |

|

| Fred Richards October 2003 Corruptisima republica plurimae leges. [The more corrupt a republic, the more laws.] -- Tacitus, Annals III 27

This issue of 'Tis Only My Opinion was

copyrighted by Adrich Corporation in 2003.

Last updated - July 6, 2008

|

|